Some day soon the stock market is going to try to trick you into doing something stupid. Don’t fall for it.

It will start as a garden-variety dip, much like the one that has unfolded over the last month, hitting the S&P 500 index with its first 5-per-cent decline of the year.

“You call that a selloff?” you might be thinking. Fair enough. Dips like this come around nearly as often as the seasons change.

iStock-1424157468

But now is the time to steel one’s resolve. Because this could easily be one of those episodes that morphs into something bigger and scarier, and there will be a guttural urge to protect yourself from the contagious turmoil.

Those who let their emotions get the best of them commit a classic mistake, one that costs investors dearly every year.

It’s easy to commit to patience and calm when stocks are rising relentlessly, as they have up until this latest stumble. An uptrend that began last October elevated the S&P 500 index by 28 per cent in large part over the market’s enthusiasm for expected interest rate cuts. The TSX, meanwhile – unloved, but along for the ride – gained 19 per cent over the same period.

But the stock market is now flirting with trouble. Valuations are high, the prospects for U.S. rate cuts are vanishing, and the Magnificent Seven group of tech giants may need a new moniker.

The American economy seems to be invincible on the back of persistent strength in consumer spending, which is keeping inflation alive and the U.S. Federal Reserve on hold.

There is now a “real risk” that the Fed will be forced to put off rate reductions until March, 2025, Bank of America analysts wrote last week. So much for the six cuts the market was pricing in at the start of this year.

That is an enormous recalibration that is working its way through capital markets. Just since the start of the year, the yield on U.S. 10-year government debt has risen from 3.9 per cent to 4.7 per cent – a level that has lately not been compatible with a booming stock market.

Some back-of-the-envelope calculations help show why that’s the case.

The S&P 500 is currently trading at about 21 times estimated earnings for the next year, which translates to a yield of 4.8 per cent. Problem is, that’s barely higher than the yield on 10-year U.S. Treasuries, which are generally considered to be “risk free.”

By this measure, investors are not being rewarded for the risk they are assuming by putting money in the stock market.

Nor are Big Tech shareholders rolling in it these days. The Magnificent Seven stocks, upon which so much of the U.S. bull market is predicated, have run out of steam.

On Thursday, Facebook parent Meta Platforms Inc. dropped by 11 per cent after the company stoked fears of an AI stock bubble.

The stock market is clearly at a critical juncture. There’s no point in anticipating a major selloff.

But let’s just say the pilot has turned the seatbelt light on. If you’re a nervous flier, prepare yourself mentally.

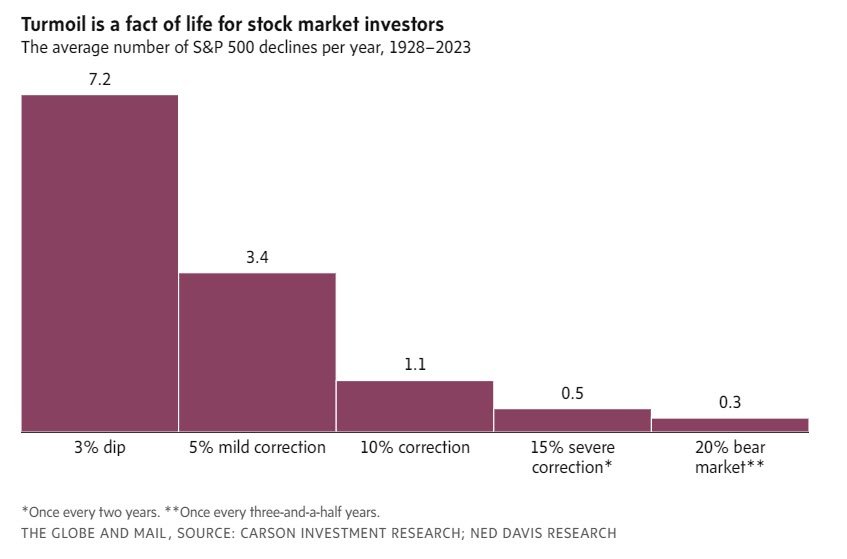

Even if this bout of volatility passes, and the bull market resumes, there will always be another big one just around the corner. Nearly a century of U.S. market data suggests that the average year has at least three 5-per-cent dips, and one 10-per-cent correction. Even bear markets, when the benchmark index falls by at least 20 per cent, happen at the surprisingly frequent rate of once every three-and-a-half years.

Your success as an investor may hinge on whether you can keep your composure when the market has lost its.

Failure to do so amounts to a kind of market timing. Investors panic and sell into a falling market in a self-defeating attempt to stem the losses, just as they get greedy and chase returns after a run of strong performance.

We’ve known for years that the average investor is a terrible market timer. This results in what has been coined the “behaviour gap” – basically the difference between what investors should do and what they actually do.

Several studies have quantified that shortfall by looking at how the average dollar in investment funds performs versus the funds themselves. Some years are worse than others. In 2021, the average equity fund investor in the U.S. underperformed the S&P 500 index by more than 10 percentage points, according to research firm Dalbar.

Longer-term studies peg the behaviour gap at somewhere between 1.5 and two percentage points per year. The same goes for the Canadian market.

That might sound minimal, but it translates to a sacrifice of about one-fifth of returns over a decade of investing. While Canadians have been rightfully badgered on the evils of investment fees, they are losing at least as much each year to bad behaviour.

There are ways to protect yourself from your own worst instincts. Investing a fixed amount each month regardless of conditions, for example. Regular portfolio rebalancing. And the counsel of a good adviser can help.

But mostly, it comes down to avoiding making rash decisions in times of crisis. In the words of index-investing pioneer Jack Bogle, “don’t do something, just stand there!”

© Copyright 2024 The Globe and Mail Inc. All rights reserved.

Comments are closed.