Bumpily and with a few shudders, central bankers made the landing in 2024. The grim predictions that only deep recessions could pull sky-high inflation back down to earth proved misplaced. Instead, a sharp increase in interest rates, supply-side improvements and the passage of time did the job well enough. Inflation is at or near 2% across the rich world and, barring trade wars or other shocks, should stay low. The economic news in most rich countries is fairly sunny. Growth varies from strong to mediocre, but at least is not negative. Share prices are still higher than ever. Unemployment is just above all-time lows.

iStock-1154857334

Job done, then? Well, almost. The economy may be back to normal, but economic policy is not. Interest rates are at their highest level since before the financial crisis of 2007-09. Most central banks—including the Federal Reserve, European Central Bank and Bank of England—started cutting rates only in the summer or autumn of 2024. Bigger drops are coming in 2025. Traders foresee roughly one percentage point of further cuts in America, Britain and the euro area.

An immediate recession does not look likely

Or look to budget deficits. America’s government is now running a deficit of 6.4%, the highest in post-war history, outside covid or the financial crash. Donald Trump will surely widen it further. Many rich-world peers have done a bit better at reining in government spending since the pandemic, though deficits also look worrisome in France and Italy.

Policy will re-normalise in 2025. Monetary policy will move faster and more consistently than fiscal policy. Central bankers tend to be more sober and predictable than politicians. Far less clear, though, is what baseline economic policy will drift back to. The last proper stretch of economic normality was five years ago. As the dust settles, what has changed?

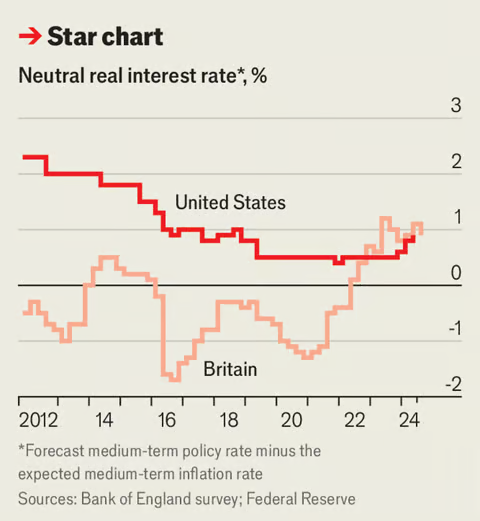

Central bankers tend to express answers to that question in terms of r* (pronounced r-star), the “neutral real interest rate”. That is the interest rate which, after stripping out inflation, neither stimulates nor depresses the economy. Alas, r* cannot be observed directly. Economists look instead at how the economy responds to real-life interest-rate moves. If the structure of the economy has changed since the pandemic, r* should be different, too.

From the 2000s to the 2010s, r* fell sharply. In the decade after 2010, even ultra-low interest rates failed to gin up demand. More recently, rich-world economies have shrugged off even quite hefty interest-rate rises. Has r* risen, and will it stay up? Jerome Powell, the Fed chair, seems to think so, as do many investors and economists (see chart). There are good reasons for this. Geopolitical tension, for instance, may have taken the shine off US Treasuries as a safe haven.

But do not call time on a low-rates world quite yet. In the long run, the single greatest determinant of real interest rates is probably economic growth. Investors can hardly expect high returns amid stagnation. Slow population growth is weighing on workforces. Growth figures were jolted around by the covid-19 pandemic, but most rich countries are either on their pre-pandemic trend or a bit below it. People who expect to live longer are likely to save more, boosting the supply of capital in search of return-generating investments. That also pushes down on r*.

As interest rates continue their descent during 2025, r* will help determine where they settle. Other factors could intervene. Rates may need to stay higher for a while to counterbalance bigger fiscal deficits if, for instance, governments raise defence spending to hedge against growing American isolationism. And if the world is now more prone to supply shocks, rate-setters may need to skew tighter to ward off inflation. But think long-term enough and r* is inescapable.

A lower-than-expected r* could cause trouble. One reason Americans have been sanguine about the recent wobbles in the labour market is that the Fed still has plenty of room to ease. But if the neutral interest rate is lower, then rate cuts will also have to be deep to push monetary policy into stimulative territory.

None of that should be a concern yet. An immediate recession does not look likely. But the further rates fall, the more likely it is that monetary policy will start feeling like the 2010s all over again.

From the 2000s to the 2010s, r* fell sharply. In the decade after 2010, even ultra-low interest rates failed to gin up demand. More recently, rich-world economies have shrugged off even quite hefty interest-rate rises. Has r* risen, and will it stay up? Jerome Powell, the Fed chair, seems to think so, as do many investors and economists (see chart). There are good reasons for this. Geopolitical tension, for instance, may have taken the shine off US Treasuries as a safe haven.

But do not call time on a low-rates world quite yet. In the long run, the single greatest determinant of real interest rates is probably economic growth. Investors can hardly expect high returns amid stagnation. Slow population growth is weighing on workforces. Growth figures were jolted around by the covid-19 pandemic, but most rich countries are either on their pre-pandemic trend or a bit below it. People who expect to live longer are likely to save more, boosting the supply of capital in search of return-generating investments. That also pushes down on r*.

As interest rates continue their descent during 2025, r* will help determine where they settle. Other factors could intervene. Rates may need to stay higher for a while to counterbalance bigger fiscal deficits if, for instance, governments raise defence spending to hedge against growing American isolationism. And if the world is now more prone to supply shocks, rate-setters may need to skew tighter to ward off inflation. But think long-term enough and r* is inescapable.

A lower-than-expected r* could cause trouble. One reason Americans have been sanguine about the recent wobbles in the labour market is that the Fed still has plenty of room to ease. But if the neutral interest rate is lower, then rate cuts will also have to be deep to push monetary policy into stimulative territory.

None of that should be a concern yet. An immediate recession does not look likely. But the further rates fall, the more likely it is that monetary policy will start feeling like the 2010s all over again.

Comments are closed.