The Bank of Canada and the U.S. Federal Reserve both began raising interest rates in March, 2022. Both tightened monetary policy at the quickest pace in decades. In Canada, that’s pushed the economy to the edge of a recession. South of the border, the U.S. economy is defying gravity.

The differences in economic performance have become increasingly stark in recent months. Canadian consumers are cutting back while Americans continue to splurge. U.S. businesses are investing in buildings and equipment, building up inventories and bringing on new workers, while Canadian companies are pulling back and bracing for a period of slow growth.

iStock-1221982108

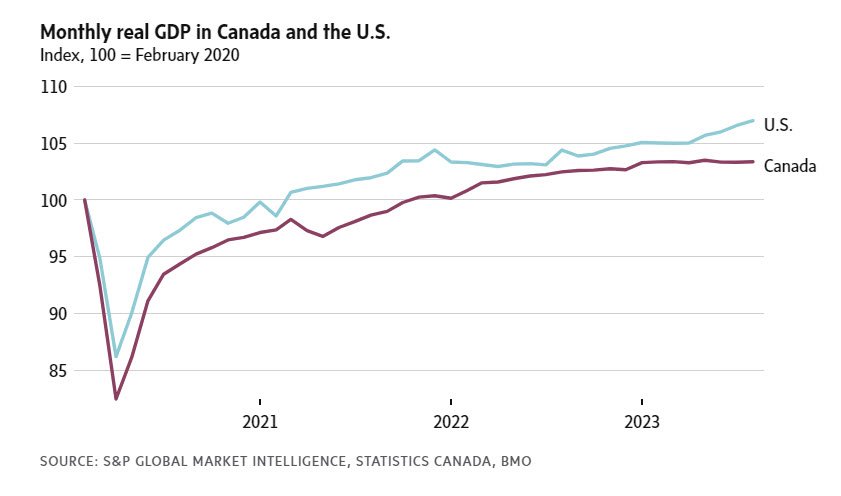

The picture is clearest when you look at gross domestic product. Canadian GDP contracted between April and June then stalled through the summer and early fall. In the United States, GDP grew at an annualized rate of 2.1 per cent in the second quarter and accelerated to a whopping 4.9 per cent in the third quarter.

What explains these divergent paths? Inflation has followed a similar trajectory in both countries, surging to four-decade highs in the summer of 2022, then declining to between 3 per cent and 4 per cent in recent months. Interest rates have moved up sharply in both; the policy rate is actually a half-point higher in the U.S. than in Canada.

But interest rates are biting more in Canada, because of higher household debt loads and mortgages that roll over more quickly. Meanwhile, the U.S. government is running proportionally much larger deficits and pumping more money into the economy. And U.S. productivity is soaring even as it slumps in Canada, adding to American outperformance.

Here are the key reasons why Canada and the U.S. are trending in different directions, and what that means for interest rates.

Canadian households hit harder by interest rates

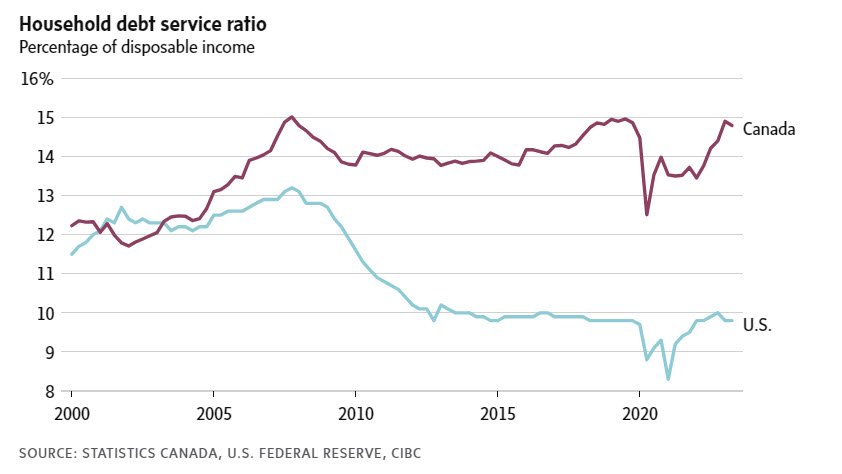

When interest rates rise, debt levels matter a lot. More money going to interest payments means less to spend on other goods and services. And Canadians are mightily indebted.

Most of this is housing debt. In the U.S., home prices crashed during the 2008 financial crisis and American households spent the next decade whittling down their debts. In Canada, home prices just kept rising, and with it the bulk of mortgage debt.

Canadian household debt was 102 per cent of GDP in the first quarter of 2023, according to the Bank for International Settlements. In the United States, it was 74 per cent.

“Even before the pandemic, even before this run up in rates, Canadians were spending about 15 cents of every after tax dollar [servicing debt], and Americans were spending about 10 cents on every dollar,” said Avery Shenfeld, chief economist at Canadian Imperial Bank of Commerce. “So the starting point was a higher interest burden, and it’s one that’s rising more sharply in Canada than it is in the U.S.”

The reason interest payments are rising more quickly in Canada has to do with how mortgages are structured. American homebuyers typically take out 30-year mortgages, allowing them to lock in interest rates for an extended period of time. In Canada, most mortgages reset every five years. That means rising interest rates are felt relatively quickly.

Since the Bank of Canada began increasing interest rates in the spring of 2022, around 40 per cent of Canadians with mortgages have seen their monthly payments increase. That proportion will rise considerably over the next few years.

A Royal Bank of Canada report published last week estimates around $900-billion worth of mortgages at Canadian chartered banks – roughly 60 per cent of outstanding mortgages on their books – will renew between 2024 and 2026.

Depending on the path of interest rates, the average monthly payments on these mortgages could jump 32 per cent next year and as much as 48 per cent in 2026, the report estimates.

In short, Canadian homeowners with mortgages (around 35 per cent of all Canadian households) are facing larger and more immediate payment shocks than their American counterparts. And that’s feeding through to the broader economy through several channels.

“It’s not just that Canadians are spending more on interest payments. They’re also choosing to save more of their after-tax income to brace themselves for those higher payments to come,” Mr. Shenfeld said.

Washington’s more aggressive fiscal policy

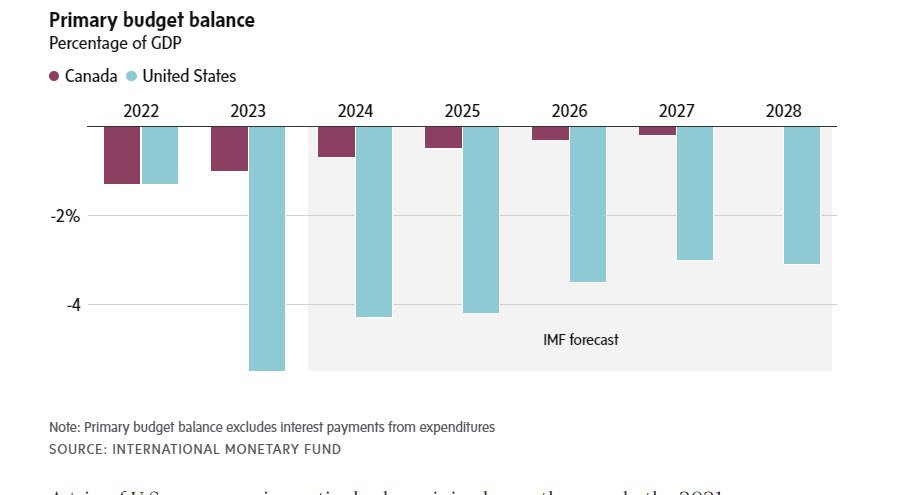

While American households are outspending their northern neighbours, so too is the U.S. government.

Both Canada and the U.S. have stimulative fiscal policies in place, but on vastly different scales. Ottawa is expected to post a deficit of more than 1 per cent of GDP this year, but Washington’s deficit is closer to 6 per cent. In the third quarter, U.S. federal spending rose 5.5 per cent annually, making it one of the fastest growing sectors of the economy.

A trio of U.S. programs in particular have juiced growth, namely the 2021 infrastructure bill, and last year’s Inflation Reduction Act and a bill supporting the semiconductor industry.

That’s showing up in heavy spending by businesses on factory construction, which is up 150 per cent in inflation-adjusted terms since the start of 2020. In Canada, investment in factory construction is only slightly up over the same time frame.

“Whether you look at just straight government spending or industrial policy incentives, the U.S. is running a much-more stimulative fiscal policy than Canada,” says Sal Guatieri, senior economist at Bank of Montreal.

Canada is pursuing its own industrial policy, like efforts to lure electric-battery manufacturers, but the pace of rollout has been slower.

“A lot of the tax measures for businesses that Canada has announced haven’t even been defined yet,” said Scotiabank economist Rebekah Young.

It’s not that Ottawa is austere. General government spending by all levels of government has grown nearly twice as fast in Canada as the U.S. since before the pandemic. It’s just that Canadian governments front-loaded their spending to the early stages of the pandemic recovery, when lockdowns were severely limiting growth, said Ms. Young.

However, while U.S. fiscal policy is helping to boost growth south of the border, it’s also creating headaches for the Federal Reserve by fanning inflation in that country.

“It’s producing stellar economic growth but at the peak of an economic cycle when the U.S. doesn’t really need it and monetary policy doesn’t welcome it,” said Mr. Guatieri.

Low productivity a drag on Canada’s economy

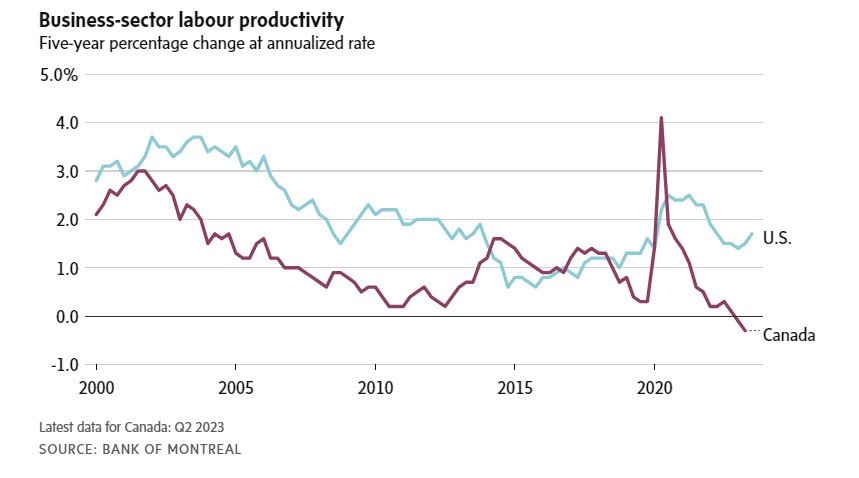

Economists and policy watchers have fretted about Canada’s languishing productivity for years. Now, it’s exacerbating the economic divergence between Canada and the U.S.

Productivity measures economic output per hour worked. If productivity was even holding steady, the surge in Canada’s population – and the increased supply of workers and demand for goods and services that comes with that – would be expected to power growth. But productivity has declined in 11 of the past 12 quarters.

In the U.S., on the other hand, productivity climbed in the third quarter by 4.7 per cent, the fastest pace in three years.

The drop in Canadian productivity reflects weak business investment in machinery and technology that would help workers do their jobs more efficiently.

“How can you explain your economy stalling in an environment of 3-per-cent population growth,” said Mr. Guatieri. “Until we turn that trend around, it’s going to be a problem for Canada’s economy.”

What does this mean for interest rates?

Many economists believe the Bank of Canada and the Federal Reserve are done raising interest rates, although the strength of the U.S. economy does increase the odds of another hike by the Fed. Speculation on Bay Street and Wall Street is shifting to when the central banks might begin cutting rates.

The relative weakness of the Canadian economy suggests that the Bank of Canada will move first, said Mr. Shenfeld: “We’re already two quarters into a stall in growth that has yet to even begin in the U.S. So in all likelihood, we’ll get some interest-rate relief before the Americans see it.”

Mr. Shenfeld’s team at CIBC is projecting the first rate cut from the Bank of Canada around the middle of next year, followed a few months later by the Fed. Interest-rate swap markets, which capture market expectations about monetary policy, are pricing in cuts by both central banks starting next summer.

If the Bank of Canada moves first, that could put downward pressure on the Canadian dollar. But Mr. Shenfeld said that should not be a major problem.

“We do expect to see a bit of currency weakness. But I don’t expect the Canadian dollar to go into a free fall, as long as the market is still anticipating at that point that the Fed will start cutting rates soon enough.”

Comments are closed.